Quick Answer: The Section 45S tax credit allows eligible small businesses to offset up to 25% of paid family and medical leave wages or commercial insurance premiums under permanent federal guidelines. To claim these savings, your business must have a formal, written policy in place, and your bookkeeping system must strictly isolate qualifying leave data from standard PTO. While your CPA calculates the final tax deduction at year-end, we need to ensure your day-to-day payroll codes and general ledger are configured to maintain an audit-proof paper trail.

Key Takeaways

- The federal employer credit for paid family and medical leave is now a permanent fixture of the tax code, meaning small businesses need a long-term, systematic approach for tracking this payroll data.

- To leverage this incentive, your business must have a written policy explicitly guaranteeing a minimum of two weeks of leave at 50% wage replacement; standard, “no-questions-asked” PTO buckets cannot be used.

- Under the permanent OBBBA updates, your bookkeeping system can now be configured to calculate the credit using either actual leave wages paid out or the commercial insurance premiums spent to fund your leave policy.

- The credit is strictly limited to employees who earned $96,000 or less in the prior year, which means your bookkeeping software must run a clean historical compensation filter before assigning specialized leave codes.

- If your business operates in a state with mandatory paid leave, your general ledger must explicitly separate the legally required state baseline from the voluntary employer top-offs eligible for the federal credit.

When life happens to your employees (whether it’s the birth of a child, a medical emergency, or a sudden family crisis), you have to figure out the logistical reality for your Milwaukie business:

How will your cash flow sustain paying a regular salary to an employee who isn’t actively working?

That’s where a federal incentive called the Section 45S tax credit can help, which can offset up to 25% of those leave costs.

And thanks to recent permanent updates under the OBBBA, the credit now offers more value for small businesses than ever.

While I don’t file your business income taxes, I want to make sure your financial systems are proactive. If you and your CPA decide to take this credit, we need your payroll codes and tracking to be flawless so they can claim it without a hitch.

What is the Section 45S tax credit?

The Section 45S tax credit, or the employer credit for family and medical leave, is a federal tax incentive designed to help small business owners offset the costs of providing paid family and medical leave to their team. The credit amount is based on a percentage of the wages you continue to pay employees while they’re out on qualified leave. It was recently made permanent by the OBBBA.

To get this credit, the IRS requires strict separation of funds. To ensure your CPA can seamlessly claim it, we have to precisely track and isolate the specific hours and wages (or qualifying insurance premiums) tied exclusively to these major life events:

- The birth, adoption, or foster placement of a child.

- Caring for an immediate family member (spouse, child, or parent) with a serious health condition.

- The employee’s own serious health crisis that keeps them from working.

- Handling family obligations related to an immediate family member’s active duty.

By setting up clean categories for these specific scenarios in your day-to-day accounting, we turn normal payroll tracking into an audit-proof paper trail for your tax preparer.

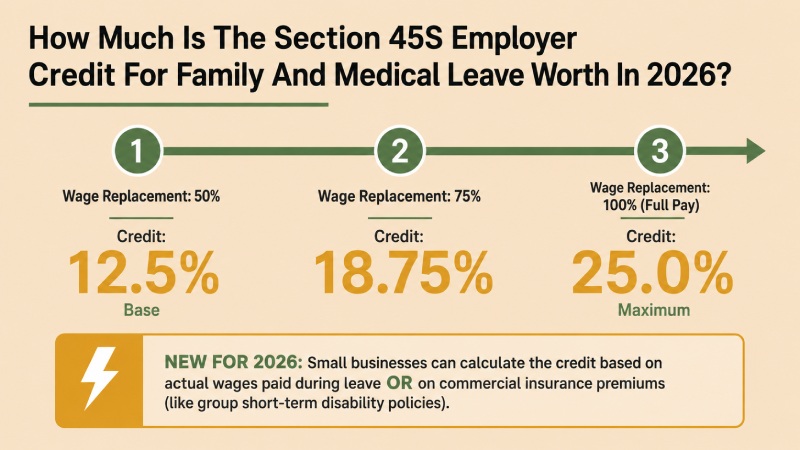

How much is the employer credit for family and medical leave worth?

The credit ranges from 12.5% to 25% of the wages you pay during your employee’s leave, for up to 12 weeks per employee per tax year.

The exact percentage depends on how much of their normal salary you cover. If you pay 50% of the employee’s regular wages while they are on leave, you qualify for the base credit of 12.5%.

For every percentage point of pay you provide above the 50% threshold, the tax credit increases. If you choose to pay 100% of their regular wages during their leave, your credit hits the maximum of 25%.

Also, thanks to the OBBBA permanent updates, your tax professional can now evaluate two entirely different tracking methods to see which one yields the best result for your cash flow:

- We track the exact hours and gross wages paid out to an employee while they are actively on leave.

- If you fund your leave policy through a commercial insurance policy (such as a qualifying short-term disability policy), the credit can actually be calculated based on the insurance premiums you pay even if no one takes leave that year.

You don’t need to stress about calculating these percentage increments or tracking the 12-week caps on your own. Once you and your CPA decide on the right policy and calculation method for your business, I’ll configure your general ledger and payroll platform so that every eligible dollar is isolated and organized for tax season.

Who qualifies as an eligible employee?

To qualify, an employee must have been on your payroll for at least one year. (Or, you can choose to lower this to six months, but one year remains the standard default.)

Also, their compensation from the prior year can’t exceed a strict federal income threshold. For the 2026 tax year, the cap restricts the credit to employees who earned $96,000 or less in 2025.

I can help you run a historical payroll report and cross-reference your team’s tenure against their 2025 gross earnings to map out exactly who qualifies.

How to write a paid leave policy

To secure this credit, you’ll need an employment attorney or HR expert to help you draft a written paid leave policy that explicitly guarantees these protections:

- The policy must offer at least two weeks of paid family and medical leave annually for full-time employees (and a prorated amount for part-time workers).

- The policy must guarantee at least 50% of the employee’s standard wages.

- The document must contain strict non-interference and anti-discrimination clauses, so employees won’t be penalized, demoted, or discouraged from using their leave.

Also, the paid leave must be specifically earmarked for Family and Medical Leave Act (FMLA) purposes.

Under the OBBBA updates, your written policy only needs to cover employees who customarily work more than 20 hours per week. This is a massive win for our bookkeeping workflow because it removes the administrative headache of setting up tracking profiles for irregular or short-hour part-time staff.

What’s the “no double-dipping” rule?

If your CPA claims the Section 45S credit for your business, they have to reduce your standard tax deduction for employee wages by the exact dollar amount of the credit you receive. And any payroll dollars we use to calculate this credit can’t be used to claim any other federal business tax credits.

From a books standpoint, this means we can’t have muddy numbers. If we don’t isolate these specific costs, your tax return and your financial books will be out of sync.

We’ll need to flag these specific payroll allocations in your accounting software so that when we hand the files to your CPA, they know exactly which dollars were utilized for Section 45S.

State vs. federal rules under the OBBBA

If your state already mandates a paid family and medical leave program, that state-mandated leave time can count toward fulfilling the federal requirement of offering at least two weeks of leave.

However, you can’t claim the federal tax credit on any mandated payments. We can only calculate the credit on the voluntary, extra compensation you pay above and beyond what the state forces you to pay.

So, if you operate in a state with mandatory leave, you’ll need to configure your payroll to track two distinct tiers of pay codes: one for the mandatory state baseline, and one for the voluntary federal-credit-eligible top-off.

That way, when tax time arrives, your CPA will have two perfectly separated buckets and can confidently maximize your federal credit without crossing any compliance lines.

Should you claim the employer credit for family and medical leave?

Before you schedule a strategy session with your Portland CPA, here are the areas I can help you evaluate to see if your business is a good candidate:

1. Your employee compensation and hours distribution. We need to audit your current payroll data to see who actually qualifies. I can generate reports to determine how many of your employees earned $96,000 or less in 2025. At the same time, we’ll analyze how many part-time employees customarily work more than 20 hours per week, since your written policy will need to cover them uniformly.

2. Your funding model. Do you want to pay wages out of pocket when someone goes on leave, or do you prefer a predictable monthly insurance expense? Because you can now claim the credit against commercial insurance premiums (like group short-term disability), I can run a comparative analysis to see which model saves you more cash while minimizing risk.

3. Your geographic footprint. Where are your employees physically located? If you have remote team members in states with mandatory paid family leave laws, I will check your payroll tax profiles to see what the state already requires you to provide. This gives us a baseline so your CPA can easily calculate the tax benefit of voluntarily adding an extra layer of employer-funded pay to trigger the federal credit.

Final thoughts

If you’re feeling a bit of administrative hesitation with these rules, don’t let that stop you from capturing these valuable savings. I’m here to help you through the process.

Just get your appointment on my calendar, and we’ll review your payroll data and make sure your ledger is up to snuff so your CPA can smoothly maximize your savings at tax time.

FAQs

“How do I track Section 45S paid family and medical leave in my payroll system?”

You must set up a unique payroll earnings code specifically dedicated to this leave (e.g., “Paid Family Leave – Sec 45S”). Don’t blend these hours into your standard sick leave or regular salary buckets. The IRS requires a completely transparent, independent paper trail separating regular wages from qualifying leave wages.

“Can my business claim the Section 45S tax credit if we use a general PTO policy?”

No, general “no-questions-asked” PTO, floating holidays, or standard vacation buckets don’t qualify for the Section 45S credit. To be eligible, your business must have a standalone, written policy that explicitly earmarks paid time off for FMLA-qualified reasons and guarantees at least 50% wage replacement.

“What employee payroll records do I need to collect for the Section 45S credit?”

To ensure your CPA can seamlessly claim the credit, your bookkeeping files should preserve a signed copy of your company’s written leave policy, employee hire dates confirming at least six months of service, prior-year W-2 gross compensation forms showing the employee earned $96,000 or less, and payroll logs detailing the dates and hours the employee spent on qualifying leave.

“How do the 2026 OBBBA updates change how we track insurance premiums for the credit?”

Under the OBBBA updates, employers no longer have to wait for an employee to take leave to see a financial benefit. If you fund your paid leave program through a commercial insurance policy (like group short-term disability), the credit can now be calculated based on the premiums you pay. Operationally, your bookkeeper will track and isolate these specific premium invoices in a dedicated line-item account in your general ledger.

“Can the employer credit for family and medical leave apply to part-time employees?

Under the OBBBA rules, part-time employees must customarily work at least 20 hours per week to qualify for Section 45S tracking. To evaluate who qualifies, we’ll need to pull a lookback hours report across the employee’s tenure to calculate their weekly average. If they average 20 hours or more, they’re mapped into the credit-eligible tracking system. If they fall below, they’re kept in standard payroll codes.

“How does the Section 45S credit impact regular payroll expense bookkeeping?”

Because claiming this credit requires your CPA to reduce your standard business tax deduction for employee wages by the exact dollar amount of the credit received, your numbers must be perfectly segregated. We can prevent year-end errors by keeping leave payroll expenses completely separated in your Chart of Accounts, allowing your tax professional to make the necessary tax adjustments without sorting through old timesheets.